Coverage that actually protects what matters most

Cassondra Sells is an independent insurance agent in Arvada, CO — shopping 60+ top carriers to find you the right coverage at the right price. Auto, homeowners, life, income & disability, commercial, and collectibles.

Get a free quote from Cassondra

Complete insurance solutions for every stage of life

Whether you're protecting your family, your home, your business, or your prized collection — Cassondra finds the right coverage from the right carrier at the right price.

Auto Insurance

Liability, collision, comprehensive, uninsured motorist, and more. Colorado requires 25/50/15 — Cassondra helps you go beyond the minimum to truly protect yourself.

Learn more →Homeowners Insurance

Denver metro averages 8–12 hail events per year. Make sure your home has replacement cost coverage, proper roof protection, and the right deductible for Colorado weather.

Learn more →Life Insurance

Term, whole, and universal life insurance. Cassondra helps Denver-metro families secure life insurance so they can live stress-free knowing they're prepared.

Learn more →Income & Disability

Short and long-term disability coverage. If an injury or illness keeps you from working, disability insurance replaces your income so your family stays financially protected.

Learn more →Commercial Auto

From moving and trucking to small business commercial vehicles — Cassondra is deeply knowledgeable in commercial auto lines. One agent handles all your Colorado commercial coverage needs.

Learn more →Moving Company Insurance

Built for movers by a former moving company owner. Commercial auto, cargo, general liability, workers comp, and FMCSA filings — structured the way moving operations actually work.

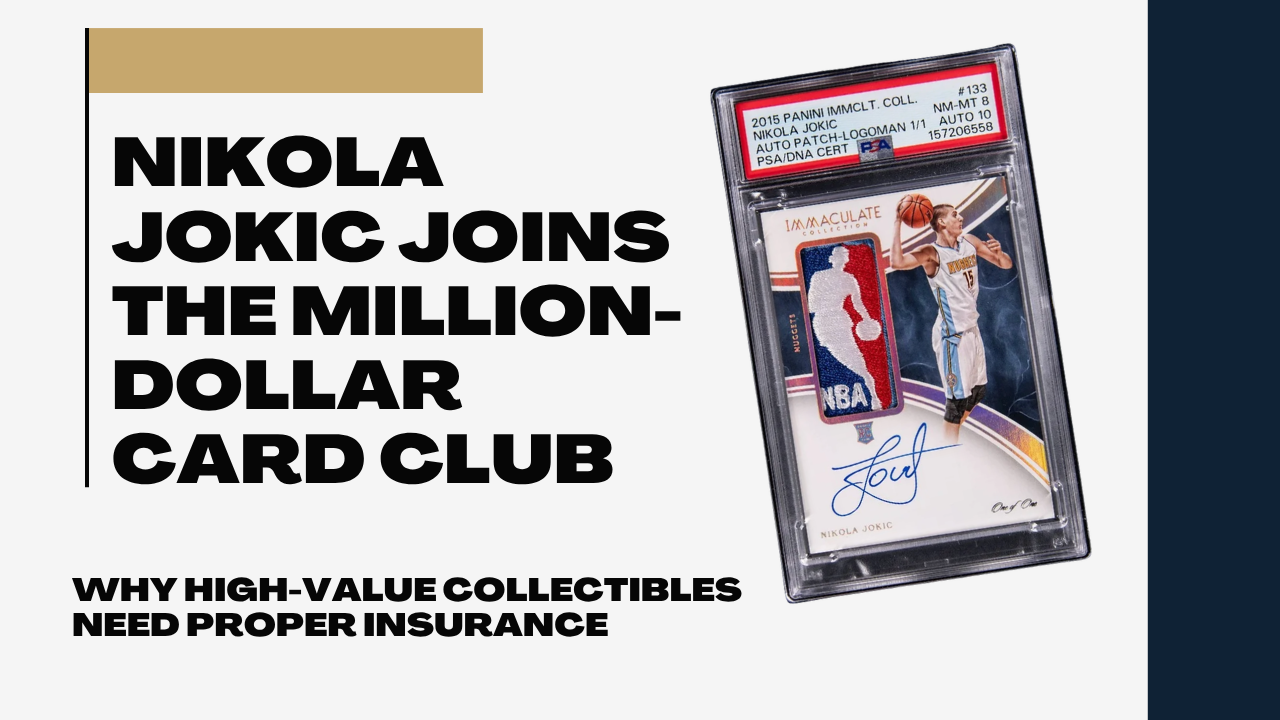

Learn more →Collectibles Insurance

Coins, cards, art, jewelry, wine, memorabilia — standard homeowners policies have low sublimits. Specialty coverage that pays what your collection is actually worth.

Learn more →The independent advantage — your advocate, not the carrier's

Cassondra works for you, not the insurance company

Unlike captive agents who can only sell one carrier's products, Cassondra is independent. She shops 60+ carriers to find the best coverage and price for your specific situation.

Colorado-specific expertise

Hail damage, wildfire risk, high-altitude weather, mountain properties — Cassondra understands Colorado's unique insurance landscape and knows which carriers perform best here.

A real person, every time

No 800-number runaround. You have a dedicated agent who knows your policy and picks up the phone when you need help — especially at claim time.

Carrier Partners

Access to 60+ carriers means you win.

Cassondra sends your information to multiple carriers simultaneously and presents you with the best options — saving you hours of research and potentially hundreds per year.

A 5.0★ rating built one client at a time

Real reviews from real Colorado clients across home, auto, life, commercial, and business insurance.

"She CARES about your needs and goals. That's the part you can't fake, and it's why I send everyone I know to Sells Insurance."

Naomi Lee

Long-time client

"Cassondra found me better coverage while actually lowering my premiums on both my home and auto. She took the time to explain everything in plain English."

Isidro Bueno

Home & Auto · Arvada

"Beyond knowledgeable in the moving and trucking industry. Cassondra got our fleet placed with the right carrier when nobody else could even quote us."

Michael Rouviere

Commercial / Trucking

"Cassondra walked us through every option for life insurance. Now I live stress-free knowing we are prepared if anything ever happens to me or my husband."

Jenny Acosta

Life Insurance

"I've worked with Cassondra for 14 years. Always reliable, thorough, knowledgeable, and kind — she treats my business like it's her own."

Melody Javaherian

Business · 14-year client

"An honest assessment of my existing policies without any sales pressure. Cassondra told me what to keep and what to change — exactly the advice I needed."

Sheila Wagner

Coverage Review

"She CARES about your needs and goals. That's the part you can't fake, and it's why I send everyone I know to Sells Insurance."

Naomi Lee

Long-time client

Latest article

Proudly serving Arvada & the entire Front Range

Based in Arvada, Cassondra serves clients across Jefferson, Adams, Arapahoe, Denver, Douglas, and Broomfield counties.

Ready to compare rates?

Get quotes from 60+ Colorado carriers in minutes — no obligation, no pressure.